Filing your US tax return as an expat isn’t exactly a walk in the park since it will require you to have a good grasp of the process, forms, requirements, and more.

Plus, because of how complex the filing procedures can get, you might make some mistakes that will be a nightmare to sort through and end up with heavy penalties.

If you don’t want to face the horrors of US tax return filing for expats, then you’ll need to know the “Fails” that you seriously need to steer clear of.

To help you do just that, here are four US tax return filing nightmares and how you can avoid them.

Let’s get started.

Table of Contents

1. Failing to file your expat US tax return in years.

If you missed the April 15 tax return filing due date or the or the June 15 automatic extension for expats, you could still request for an extension until October 15.

Keep in mind, though, that you still need to pay the value of your tax returns on time; otherwise, you’ll be paying interest and penalties.

However, failing to file and pay your expat tax return in years can result in bigger penalties, and you will have to determine the equivalent amount of back taxes you need to file and pay.

Plus, you’ll need to prepare all the documentation you need to complete the required reports and returns to be compliant with the IRS.

This could mean a long and painful process, but the good news is, the best step you can take to avoid it is to file your taxes on time.

To help ensure that you file your expat tax return within the deadline, you’ll need to have the necessary documents and forms – such as Form 1040 ready.

If you do find yourself in a situation where you’ve gone way past the tax return due date, you can still file and use streamlined procedures.

With the Streamlined Foreign Offshore Compliance Procedures, you can catch up on your delinquent returns by filing only the last three years of your late expat tax returns, including six years of Foreign Bank Account Reporting forms and a questionnaire.

2. Not complying with Foreign Bank Account Reporting (FBAR)

There are small mistakes you can make when it comes to filing your US tax returns – such as not knowing how to deduct business expenses on your federal taxes – but there are also critical errors that you seriously need to avoid making at all costs.

If you are a US citizen who has or owns signature authority over financial accounts overseas – including foreign branches of banks who have headquarters in the US – then you are required by the IRS to file the FBAR form.

The reporting threshold for you to file FBAR is if the value of all your foreign accounts exceeds $10,000 at any time throughout the year.

If you fail to comply with this mandatory form, you can face severe penalties of up to $12,000 for each non-willful violation.

For willful violations, though, you could be looking at a penalty of around $124,000 or fifty percent of the balance in your account – whichever amount is higher.

Now that’s a nightmare come true that you wouldn’t want to be stuck in.

To avoid getting penalized, you’ll need to file your FBAR if you meet the qualifications for it.

Here are the three best tax filing services that you can file

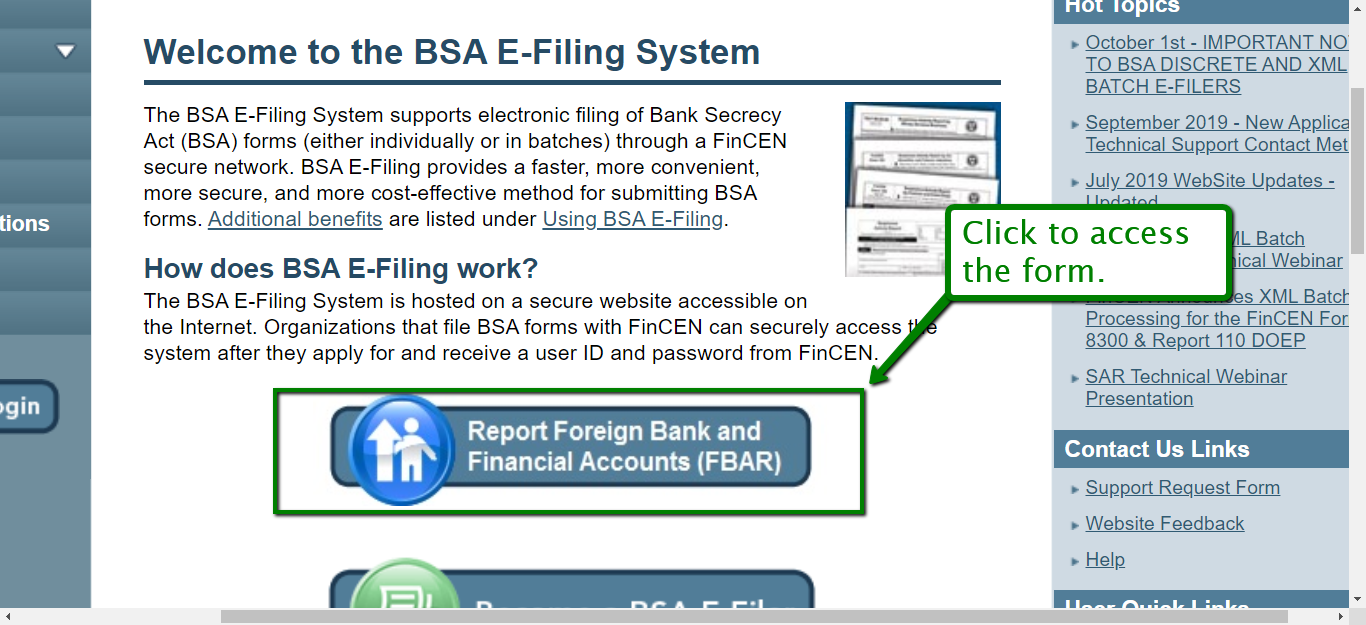

- Electronic filing. The IRS requires you to file your FBAR electronically through the BSA E-Filing System of the Financial Crimes Enforcement Network (FinCEN).

Just go on the website and click on the FBAR form button. Keep in mind that you don’t file this with your federal tax return.

- Paper Filing. If you choose to paper-file, you’ll need to call the FinCEN Regulatory Helpline and request for an e-filing exemption and wait for your approval.

- Filing on your behalf. You can have someone else file your FBAR on your behalf using the FinCEN Report 114a to authorize the other person to do so.

3. Non-submission of the Statement of Specified Foreign Financial Assets (Form 8938)

You are required to file your Statement of Specified Foreign Financial Assets (Form 8938) with your federal tax return if (at the end of the calendar year) your specified financial assets reach over $200,000.

Be warned, though, that not filing this form will result in a $10,000 penalty that could reach up to $50,000.

Plus, if you don’t declare on your tax return your income relating to your specified foreign assets, you’ll get a 40% on your attributable tax.

Your solution to avoid getting penalized then would be to look at the conditions that will determine whether or not you need to submit Form 8938.

You can also go on the IRS.gov website to get an electronic copy of the form and complete filing instructions.

If you’re unsure if you need to file Form 8938, take a look at some of the conditions.

- You have interests in specified foreign financial assets that need to be reported.

- You are a specified person, either a domestic entity or a specified individual.

- The accumulated worth of your specified foreign financial assets exceeds the reporting thresholds applicable to you.

Once you establish that the conditions apply to you, start gathering all the other forms and documents required so you can file this form along with your federal tax returns.

4. Claiming for the foreign earned income exclusion incorrectly.

You might consider claiming the Foreign Earned Income Exclusion (FEIE), so you can exclude the about $100,000 (figures can differ from each year) of your income from being taxed.

However, you can make some of the common mistakes that many expats also commit when claiming the FEIE.

Here are a few of them.

- You’re not sure what type of income does or doesn’t qualify.

- You incorrectly calculate the days that you spent outside the US.

- If you fail to provide enough evidence to pass the Bona Fide Residence Test.

- If you don’t look for other options – such as claiming the Foreign Tax Credit instead of the FEIE – that will give you more benefits.

Making these mistakes can get your FEIE claim denied, which can lead to getting double taxation for you.

One of the best ways to ensure you don’t make the mistakes mentioned above and avoid double taxation is to work with US expat tax professionals.

Doing so can help you make sure you file your taxes on time and have the peace of mind of knowing you’re working with experts who can make the process smoother and more efficient.

Final Thoughts

Filing your US expat tax return can be confusing and challenging, but it doesn’t have to be that way.

By knowing the possible horrors you can face when filing your tax returns and learning from them, you’ll be better equipped to make the process less painful for you.

Although there are more US tax return horror stories you can gain insights from, considering the four discussed here is definitely a step in the right direction.

If you learned something from this guide, please share it with your network. Cheers