Despite every effort of spreading awareness about personal health insurance policies, a significant number of Indians still depend on their corporate or group health insurance plans for medical security. A majority of working individuals today are young and have not yet experienced any medical problems that might put a strain on their pockets. They think their family members are secure due to the provision for dependents in the corporate health plan.

Mr. Kapoor is a 30-year old who lives in Delhi with his wife and a 3-year old son. His company provides a corporate health plan which comes at nominal premium rates and has till now offered benefits in maternity and baby care without any waiting period. So, the family has remained financially secure till now without any medical costs affecting them personally. But, will this continue beyond a certain age? It might seem possible today,but, one can never guarantee such things in future at the age of 40 or 50 and beyond.

Considering the lifestyle changes and the rising medical costs, which reportedly have become a double-digit figure in the past few years, even more than the average inflation rate of the country, it is best suited for an individual to avail a personal health insurance policy and not depend on the one provided by the employer. This becomes more significant for those who live in a joint family.

There might be a lot of benefits that a group cover might provide like no waiting period, no burden to pay the premium and no requirement for a medical check-up before availing the policy, but at the same time, one needs to look beyond a limited cost and time coverage to remain financially secure for the entire life.It is important to remain aware of the benefits of a family health insurance cover over a group policy in terms of covering any medical emergency or critical ailments.

Group Mediclaim Policy vs. Family Health Plan

|

Factors |

Group Health Insurance | Family Health Insurance |

| 1. Customisation | As it is bought by a company, it is not possible to customise the policy as per the requirements of policyholders. | It can be customised according to the requirements of the family. |

| 2. Coverage | This policy often provides a limited cover (Rs 2-4 lakhs) to the employee and his/her dependents.

There might be no coverage for parents in some group health plans. |

The amount or sum insured can be decided on the basis of personal requirements.

This policy covers all the family members. A separate health plan for parents is also available. |

| 3. Rider Plans | It is a uniform policy and no employee can avail any rider on it unless provided by the employer. |

Riders can be bought by an individual as per the needs. It depends on the policyholder if he/she wants to avail top-ups or super top-ups to increase cover at nominal premium rates.An employee can also avail a critical illness rider plan to cover any An employee can also avail a critical illness rider plan to cover any critical ailments in the future. |

| 4. Job Switch | The policy will not offer coverage if the employee leaves the job. In this case, if the new employer does not provide any health cover or offers a cover lesser than the previous one, then the individual might suffer. | There is no effect on a health insurance plan due to job switch. |

| 5. Cost-cutting | In case of cost-cutting, this is a benefit which the company might reduce or withdraw.

|

The family health plan will not be discontinued even if the insured is trying hard to save money.. |

| 6. Retirement | Most companies do not offer any health cover to their retired employees.

In such a case, a person will remain without any medical coverage after retirement. |

Most of the individual health insurance plans come with a lifetime renewability feature. It means, the policy will offer coverage even after retirement. |

In addition to this, many corporate health insurance policies have additional clauses, like co-payment and deductible in order to cut costs. It means, a substantial amount of cost has to be borne by an employee itself.

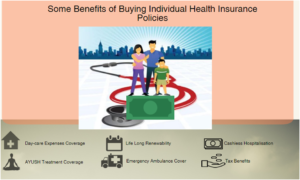

It can be clearly seen that a family health plan is much better to avail as it provides one more choice in the long-term than a corporate health insurance policy. Please add it to your insurance portfolio as it is quick and easy to buy a health insurance plan online. Moreover, mediclaim policies are portable.

As medical inflation, has increased at an unprecedented rate, it is necessary to buy an individual health insurance policy.